Green Mortgage Lawyers | Market Insights | June 2026

The Australian mortgage lending market is not heading into a collapse. It is heading into a recalibration. And that distinction matters.

Because while headlines continue to scream about cost of living pressures, housing affordability, global instability, tax reform, rising interest rates, and interest rate uncertainty, something more significant is happening beneath the noise:

{kind=link}

Money is not disappearing. It is moving.

Moving into different asset classes. Different property investment strategies. Different lending products. Different borrower behaviour. Different risk appetites.

For lenders, mortgage brokers, legal lending professionals, and financial advisers, this is the moment that separates reactive businesses from strategic ones.

The Federal Budget may have sparked debate across every dinner table in Australia, but the deeper impact will not be measured in headlines over the next few weeks. It will unfold slowly through borrower confidence, lending appetite, investment behaviour, servicing pressure, property market activity, and policy reform over the coming years.

And while everyone seems focused on what could go wrong, the real question is this: Where will lending flow next?

The Lending Market is not Frozen. Borrowers are Becoming More Calculated.

Australians are not walking away from wealth creation. They are simply becoming more cautious, more strategic, and more selective about where they place their money.

That changes the shape of mortgage lending and property finance.

Borrowers are reassessing risk. Investors are questioning traditional investment property strategies. Families are prioritising security and liquidity differently. Younger Australians are approaching property ownership and home loans with a completely different mindset than previous generations.

At the same time, lenders and mortgage brokers are navigating a market where borrower circumstances can shift dramatically between loan approval and settlement.

The “set and forget” lending environment is gone.

This is now a market that demands agility, structure, communication, and stronger execution discipline across the entire mortgage lending lifecycle.

So What Lending Products Are Proving Resilient?

In uncertain markets, flexibility wins. We are seeing continued resilience in lending products and loan structures that allow borrowers to adapt to changing economic conditions rather than become trapped by them.

Offset accounts, redraw flexibility, interest-only investment loans, SMSF lending structures, and lending products supporting long-term asset retention strategies continue to hold relevance because borrowers want optionality.

Commercial property lending also remains active, but the deals moving forward are typically more structured, more scrutinised, and more strategically positioned.

The appetite for lending has not disappeared. The tolerance for poorly structured mortgage and commercial lending deals has. That is a critical distinction for lenders, mortgage brokers, and legal lending teams alike.

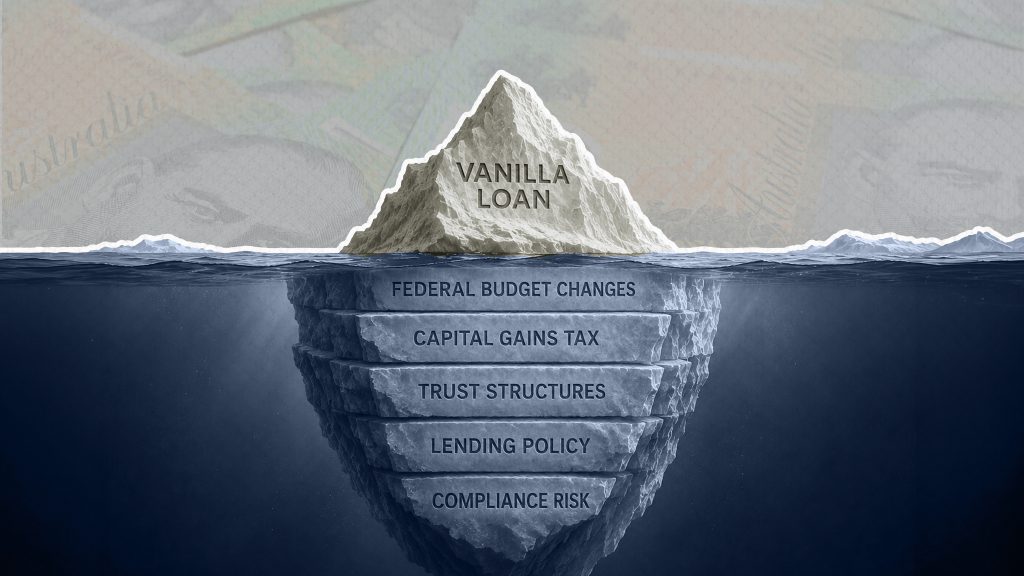

Negative Gearing, Discretionary Trusts and Investment Structures in Australia: What Still Works?

Every time there is policy uncertainty or Budget reform discussion, the same questions resurface: Is negative gearing finished? Do discretionary trusts still work? Should borrowers abandon property investment strategies altogether?

The reality is far less dramatic. Sophisticated investors do not typically abandon wealth creation strategies overnight. They adapt them. Legal structures still matter. Asset protection still matters. Tax effectiveness still matters. Estate planning still matters. What changes is how borrowers use those structures and how carefully lending needs to be assessed around them.

Discretionary trusts may continue to play a role for many borrowers, particularly where flexibility and asset management remain important. Negative gearing may become less attractive in some scenarios if reforms tighten further, but that does not automatically eliminate property investment demand or investment lending activity.

It simply means borrowers, lenders, mortgage brokers, and advisers need to become more strategic, more educated, and more deliberate in how lending deals are structured.

And importantly, lenders need to ensure their lending products, lending policies, and servicing assessment models keep pace with the changing reality of modern borrowers.

Home Loans, Superannuation and Property Investment: The Rise of the Security First Investor

One of the most significant shifts emerging from the current economic environment is psychological. Australians are becoming increasingly security focused. For many, superannuation and the family home are once again being viewed as the safest long term pillars of wealth creation.

That mindset shift matters enormously to the mortgage lending sector. Because when borrowers become more conservative, lending behaviour changes with them. We may see stronger demand for home loan products that prioritise stability, certainty, lower risk exposure, and long-term asset retention rather than aggressive short-term growth strategies.

At the same time, there will still be investors actively seeking opportunity during uncertainty, particularly in commercial property, strategic acquisitions, distressed property opportunities, and alternative investment markets.

History has shown repeatedly that periods of economic pressure often create enormous opportunity for borrowers, lenders, and businesses prepared to move decisively while others hesitate.

Mortgage Lending Risk and Settlement Delays: Why Execution is the Biggest Challenge in 2026

In this market, the greatest danger is not always the interest rate itself. It is execution failure.

A borrower approved six weeks ago may now have different living expenses, altered cash flow, changed liabilities, or increased financial pressure by the time loan documents are issued and settlement approaches.

That means lenders and mortgage brokers cannot simply focus on loan approvals anymore. They must focus on settlement certainty.

Strong communication, efficient document management, structured workflows, fast turnaround times, and real time visibility across property finance transactions are becoming increasingly critical in protecting lending outcomes.

This is where operational discipline matters. The firms, lenders, brokers, legal lending teams, and mortgage professionals that succeed in the next phase of the market will not necessarily be the loudest.

They will be the most responsive, strategic, and execution-focused.

What Mortgage Brokers and Lenders Should be Doing Right Now to Navigate the Changing Lending Market

Not panicking. Preparing. This market does not reward hesitation. It rewards strategy, visibility, communication, and execution.

For lenders and mortgage brokers, now is the time to tighten processes, strengthen borrower relationships, and reassess how deals move from instruction through to settlement in an environment where borrower circumstances can shift rapidly.

1. Review Lending Products Against Current Borrower Behaviour

Borrowers are thinking differently. Lending products need to reflect that reality.

Many Australians are prioritising flexibility, cash flow management, and long-term security over aggressive growth strategies. This is the time for lenders to assess whether their current product offerings still align with modern borrower expectations and market conditions.

Ask:

- Are products offering enough flexibility?

- Are servicing models still realistic in the current economic climate?

- Are borrowers being set up for sustainability, not just approval?

Lenders that evolve with borrower behaviour will remain competitive as the market recalibrates.

2. Strengthen Borrower Communication and Education

Confidence is built through clarity. Borrowers do not need more fear driven commentary. They need guidance, transparency, and practical support from professionals who understand the market beyond the headlines.

Mortgage brokers and lenders should be proactively educating clients around:

- Interest rate movements

- Refinancing strategies

- Cash flow management

- Investment structure considerations

- Changing servicing expectations

- Settlement timelines and documentation requirements

The businesses that communicate clearly during uncertain markets are the businesses that build long-term trust and client loyalty.

3. Improve Visibility Across the Mortgage Lending Lifecycle

One of the biggest risks in the current market is what happens between approval and settlement.

Borrower circumstances can change quickly. Delays, missing information, documentation issues, and communication breakdowns are creating unnecessary pressure across transactions.

Now is the time for lenders and brokers to strengthen:

- Transaction tracking

- Real time updates

- Workflow visibility

- Communication touchpoints

- Turnaround times

- Document management processes

The more visibility there is across a deal, the faster issues can be identified and resolved before they become settlement problems.

4. Reassess Loan Servicing and Risk Monitoring Processes

The lending market has shifted dramatically over the past few years and servicing pressures continue to evolve. Lenders and brokers should be reviewing whether their assessment models properly reflect:

- Rising living expenses

- Changing borrower spending patterns

- Interest rate sensitivity

- Self employed borrower volatility

- Commercial lending complexity

- Changing investor behaviour

This is not about tightening lending for the sake of it.

It is about making smarter, more sustainable lending decisions that protect both borrowers and lending outcomes over the long term.

5. Identify Operational Bottlenecks Before They Become Settlement Delays

Speed still matters in lending. But smart execution matters more. Many transaction delays are no longer caused by one major issue. They are caused by multiple small inefficiencies compounding throughout the process.

Now is the time to identify:

- Workflow gaps

- Duplication of tasks

- Communication delays

- Outdated systems

- Slow document turnaround

- Manual processing inefficiencies

Operational discipline is becoming one of the strongest competitive advantages in the mortgage lending sector.

6. Focus on Strategy, Not Short-Term Reaction

Markets move in cycles. Fear does too. The Lenders and Mortgage Brokers who will thrive over the next few years will not be the ones reacting emotionally to every headline or Budget announcement.

They will be the ones who stay informed, remain agile, communicate consistently, and continue strengthening their processes while others retreat.

Because in uncertain markets, borrowers are not simply looking for a transaction. They are looking for confidence, certainty, and trusted guidance.

The Lending Market Ahead Will Reward Strategy Over Speed Alone

There is no question Australia is entering a more complex economic chapter.

Budget pressures, geopolitical instability, inflation, rising interest rates, housing affordability challenges, property market uncertainty, and shifting taxation policy will continue to influence borrower behaviour for years to come.

But markets evolve. They do not stand still. And while some sectors may experience pain, others will create opportunity. The mortgage lending market ahead will belong to those who understand risk properly, structure lending deals intelligently, communicate clearly, and move with discipline.

Because in uncertain times, trust becomes currency. And experience, strategy, execution, and settlement certainty become more valuable than ever.